One warm patch of water in the Pacific Ocean can travel much farther than it looks on a map. In 2026, El Niño is again moving into the risk conversation, with potential effects on India’s monsoon season, flood conditions in parts of China, and the loss ratios of insurers and reinsurers far away from the fields and river basins where the damage first appears.

The World Meteorological Organization has signalled a likely return of El Niño conditions from mid-2026. For insurance, this is not only a climate update. It is a reminder that one ocean cycle can place pressure on agriculture, flood exposure, public budgets, and reinsurance portfolios at the same time.

What El Niño means, in plain terms

The name El Niño comes from Spanish. It means “the little boy” and, in this context, refers to the Christ Child. Fishers along the Pacific coast of South America used the name because unusually warm waters often appeared around Christmas. What began as a local observation later became the name for a wider climate pattern in the tropical Pacific.

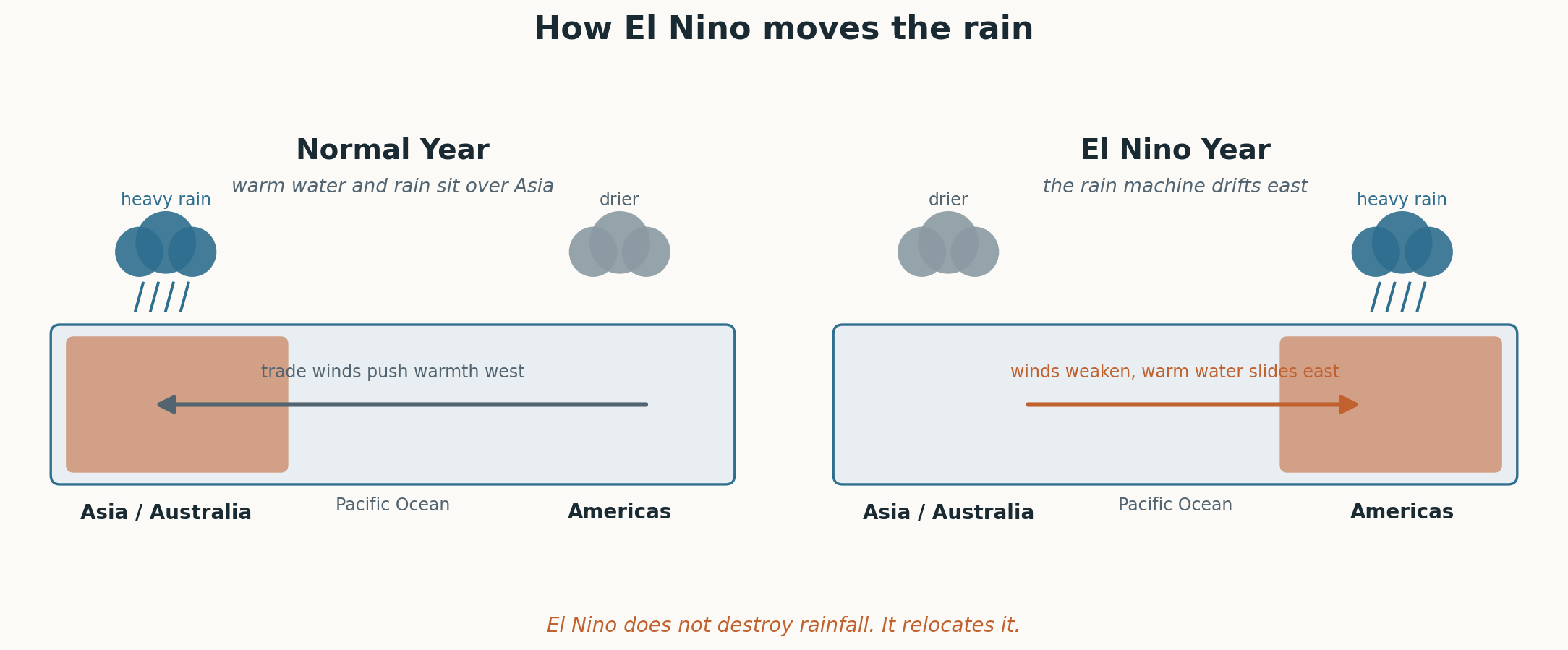

Scientifically, El Niño is the warm phase of the El Niño-Southern Oscillation (ENSO), the natural cycle that shifts between El Niño, La Niña, and neutral conditions. A simple way to picture it is a long bathtub of warm water. In a normal year, trade winds push warm water toward Asia and Australia, helping feed rainfall there. During El Niño, those winds weaken and the warm water slides east. The rain machine moves with it.

The key point is that El Niño does not simply mean “drought”. It relocates rainfall. Some regions can become drier while others face heavier and more concentrated rain. It also shifts probabilities rather than guaranteeing outcomes. Irrigation, drainage, reservoirs, river systems, urban planning, and preparedness still decide how large the final loss becomes.

India: When the Monsoon Tests Crop Insurance

India’s El Niño exposure mainly runs through the southwest monsoon. For millions of farmers, a weak monsoon is not just a rainfall issue; it can affect yields, cash flow, food prices, rural demand, and eventually crop-insurance claims.

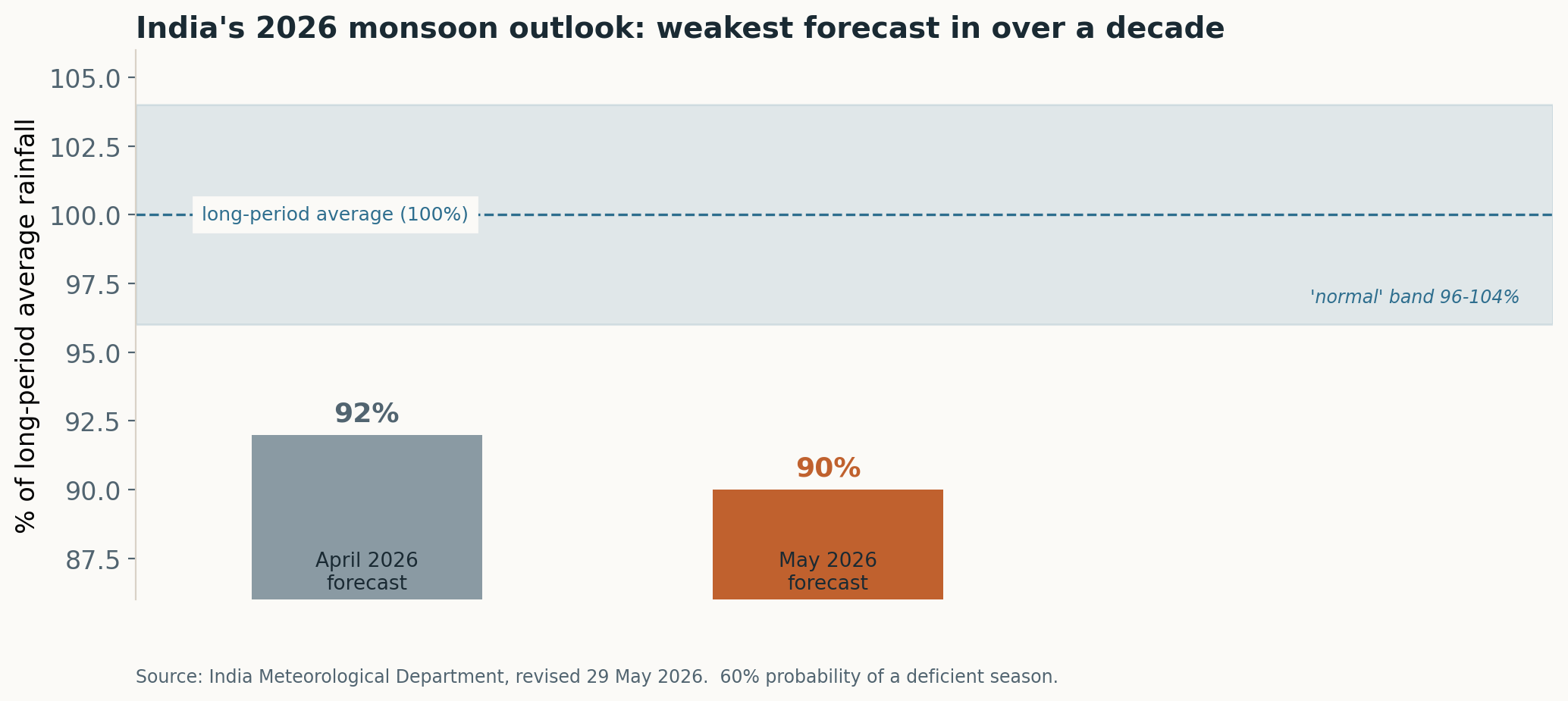

That is why the 2026 outlook matters. On 29 May 2026, the India Meteorological Department revised its seasonal forecast to 90% of the Long Period Average (LPA), below the normal band of 96% to 104%. It also assigned a 60% probability to deficient rainfall. This is not a certainty, but it is a serious risk signal.

India’s Pradhan Mantri Fasal Bima Yojana shows the scale of the protection challenge. Between 2016 and 2023, insurers collected roughly US$24 billion in premiums and paid around US$17 billion in claims. But the settlement picture is just as important. Claims paid reportedly reduced from around US$3.5 billion in FY2018–19 to about US$1.25 billion in FY2023–24. Out of 568 million farmer enrolments, around 232 million had received settled claims as of March 2024.

The remaining enrolments should not automatically be read as unpaid valid claims. Some farmers may not have suffered an insured loss in that season, while others may have been affected by assessment, documentation, yield estimation, state-level coordination, or payment-processing delays. That distinction matters. The issue is not only how many farmers are enrolled but also how quickly eligible losses are identified, confirmed, and paid.

The point is not to weaken the case for crop insurance. It is the opposite. In a weak monsoon year, insurance must be more than cover on paper. The real test is whether assessment, settlement, and payment are fast enough to support farmers while the income shock is still fresh.

Better rainfall data, satellite crop monitoring, clearer triggers, and faster claims processes can turn crop insurance from delayed compensation into a real resilience tool.

China: flood and drought can sit inside the same season

China is a different kind of El Niño problem. The same climate cycle can increase flood pressure in parts of southern China, including the Yangtze basin, while heat or dryness affects other farming regions. In insurance terms, that means flood exposure and agricultural stress can sit inside the same season.

The impact is not limited to crops. River-basin flooding can affect transport, infrastructure, hydropower, property, business continuity, and public recovery spending. At the same time, dryness or heat can pressure wheat, corn, soybeans, and other spring-sown crops.

China’s agricultural insurance penetration is a clear strength. But high coverage does not mean low volatility. PICC Property and Casualty reported around US$7.6 billion in agriculture-insurance revenue in 2024. Its agriculture loss ratio stood at 84.2%, while the combined ratio reached 99.7%. In simple terms, the combined ratio shows how much of each premium dollar is used for claims and operating costs. A ratio close to 100% means the underwriting margin is very thin. The company also handled more than 180 million agriculture-related claims, about 32% higher than the previous year.

That is the insurance lesson. A market can be well covered and still come under pressure when weather losses become frequent, severe, or correlated.

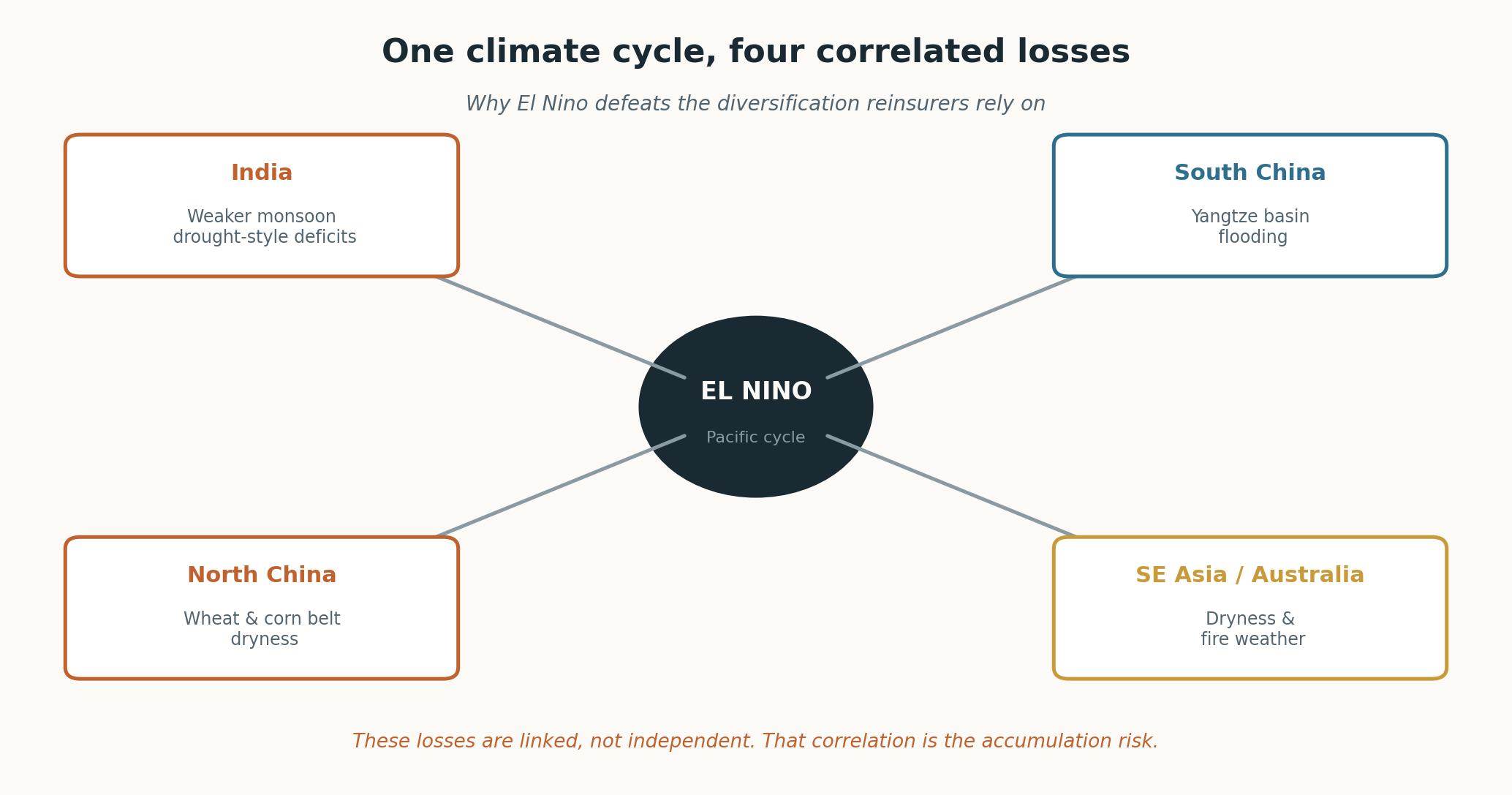

For reinsurers, China matters because the exposure is layered. Southern floods, northern crop stress, infrastructure losses, and public recovery costs can all emerge from the same climate cycle. Under El Niño conditions, that is not just coincidence. It is a correlation appearing on the balance sheet.

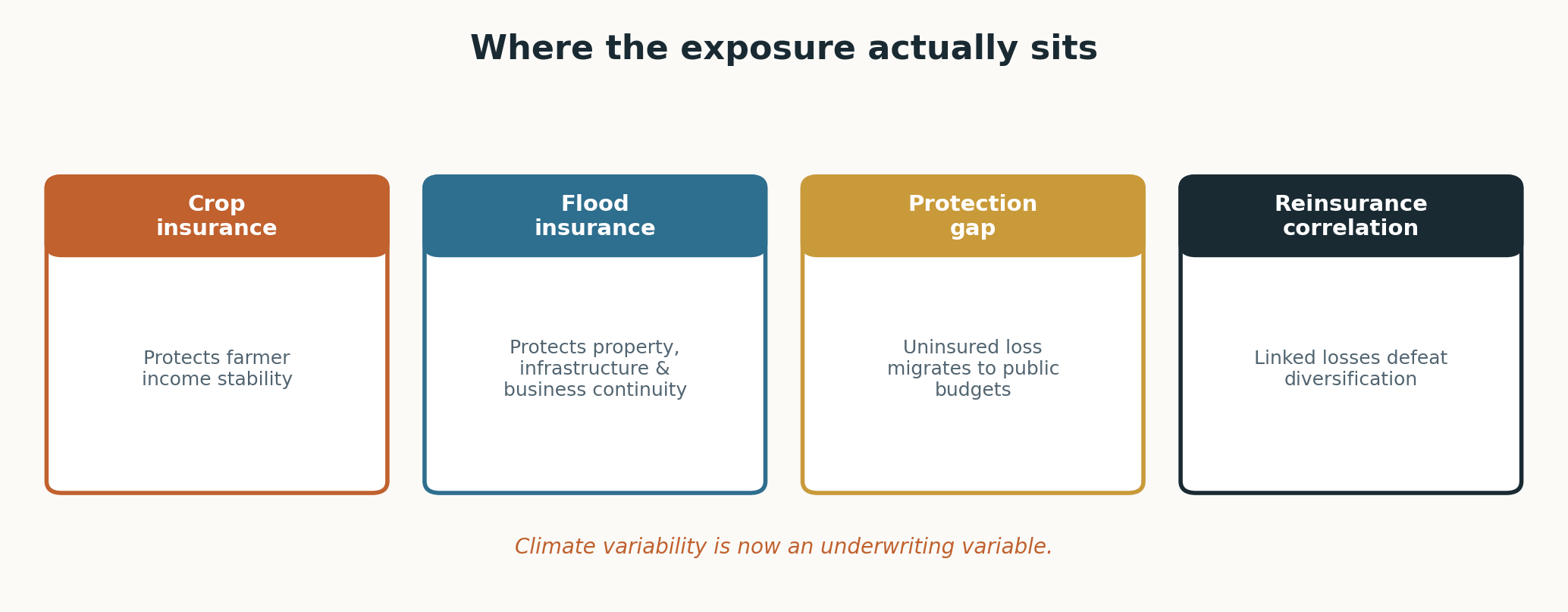

Where the exposure actually sits for insurers

Once the meteorology is stripped back, four practical insurance themes remain.

First, crop insurance protects income stability. It can help turn a failed season from a household crisis into a managed financial loss, while supporting rural credit and consumption.

Second, flood insurance protects more than buildings. It supports infrastructure recovery, business continuity, supply chains, and public finance. When floods are uninsured or underinsured, the economic loss still exists; it simply moves elsewhere.

Third, the protection gap becomes a public liability. The protection gap is the difference between total economic loss and the portion actually insured. When that gap is wide, recovery costs often migrate to households, lenders, businesses, and government budgets.

Fourth, reinsurers face correlation rather than coincidence. Reinsurance works best when losses are diversified. But a single El Niño can stress Indian agriculture, southern China flood exposure, Southeast Asian dryness, and Australian fire weather in the same cycle. These losses are linked, and linked losses are harder to diversify.

What works best from an insurance perspective

El Niño cannot be prevented, but the financial shock can be better managed if insurance is designed around early warning rather than late reaction.

For India, the priority is crop-insurance responsiveness. A weak monsoon can damage farmer income before a traditional loss assessment is fully completed. This is where rainfall data, satellite crop monitoring, soil-moisture tracking, and clearer claim triggers become important. The goal should be simple: identify eligible losses earlier and move payments faster, so crop insurance works as income protection rather than delayed compensation.

For China, the priority is accumulation management. Flood pressure in the south, crop stress elsewhere, infrastructure exposure, and public recovery spending can all develop in the same season. Insurers and reinsurers need better flood maps, crop exposure data, river-basin monitoring, and scenario modelling to understand where losses may concentrate before they appear in the claims numbers.

Parametric insurance can support both markets where speed is critical. These policies pay when a pre-agreed trigger is met, such as rainfall deficit, river level, wind speed, heat threshold, or soil moisture. That can reduce delay because payment is linked to a measurable event rather than a long physical loss assessment. The World Bank’s disaster-risk financing work describes parametric insurance as a model where payouts are made when pre-defined triggers are met, and such products can provide rapid disbursement after a triggering event.

But parametric cover is not a magic solution. The trigger must closely match the actual loss; otherwise, there can be basis risk: a payout may be too small, too large, or may not happen even when damage is felt locally. That is why the better answer is not “replace traditional insurance” but combine traditional cover, parametric layers, better data, and public-private support.

For reinsurers, El Niño should be treated as an accumulation signal. Swiss Re’s ENSO agriculture work is aimed specifically at underwriters, actuaries, reinsurance buyers, and brokers because El Niño and La Niña can affect agricultural production and insurance portfolios. Munich Re also cautions that historical statistics alone are not enough when natural climate cycles are changing the loss picture.

The practical insurance lesson is clear: use forecasts earlier, monitor exposures more closely, settle eligible claims faster, and structure reinsurance for linked losses rather than isolated events. El Niño is not only a weather signal; it is an underwriting, claims, and accumulation-management signal.

The takeaway

El Niño is not just a weather story. It is a test of how well risk is shared between farmers, insurers, reinsurers, and the state when climate variability becomes sharper. The warm Pacific water will do what it does. The insurance question is whether protection is fast enough, wide enough, and fairly priced enough to absorb the shock before it reaches a household or public balance sheet.

Climate variability is now an underwriting variable. El Niño is a useful reminder that one ocean cycle can connect agriculture, floods, public finance, and reinsurance accumulation in ways that are easy to miss when each exposure is viewed separately.

Sources and reference points

These are the institutional sources and reports used to ground the article and figures.

- World Meteorological Organization (WMO). El Niño / La Niña updates and Global Seasonal Climate Update, including the April 2026 signal that El Niño conditions were likely to develop from mid-2026.

- National Oceanic and Atmospheric Administration (NOAA), Pacific Marine Environmental Laboratory. Explanation of El Niño, its mechanism, and the origin of the name, including the Spanish meaning “the little boy” / Christ Child and the Christmas timing of the warm waters.

- India Meteorological Department (IMD), Ministry of Earth Sciences / Press Information Bureau. Updated Long Range Forecast for the Southwest Monsoon Seasonal Rainfall during June–September 2026, released on 29 May 2026.

- Reuters reporting on India’s 2026 monsoon outlook, including the economic relevance of a weaker monsoon, agriculture exposure, inflation risk, and the importance of monsoon rainfall to non-irrigated farmland.

- China National Climate Centre and China Meteorological Administration, with Reuters reporting on May 2026 seasonal briefings about El Niño development, rainfall south of the Yangtze, higher temperatures, flood risk, drought risk, and possible disruption to late-season rice harvests.

- Food and Agriculture Organization of the United Nations (FAO). El Niño anticipatory action and food-security reporting on staple-producing regions exposed to climate shocks.

- World Bank. Global Index Insurance Facility and Disaster Risk Financing and Insurance Program, including reference material on index-based and parametric climate cover, disaster-risk financing, and faster financial protection after climate or natural-disaster shocks.

- Aon. 2024 Climate and Catastrophe Insight reporting on Asia-Pacific natural-catastrophe losses and the low insured share of many regional disasters.

- Munich Re. El Niño and natural climate-cycle risk insights, including the warning that historical averages alone are not enough for climate-risk management.

- Swiss Re Institute. ENSO and agriculture: exploring the risks for insurance portfolios, a reference for underwriters, actuaries, brokers, reinsurance buyers, and reinsurers on how El Niño / Southern Oscillation can affect agriculture and insurance portfolios.

- Allianz Re. Agriculture Insurance in Asia: Protection Gap and Embracing Technology, including discussion of agricultural insurance penetration, protection gaps, and agriculture-insurance premium development in India and China.

- Pradhan Mantri Fasal Bima Yojana (PMFBY) / Ministry of Agriculture and Farmers Welfare. Official information on India’s government-backed crop-insurance scheme and government reporting that 56.80 crore farmer applications were enrolled and more than 23.22 crore farmer applicants received claims during the first eight years of implementation.

- Down to Earth. “When crop insurance fails farmers: PMFBY needs a rethink,” used for the updated India section’s PMFBY figures, including premiums collected of ₹1,97,657 crore, claims paid of ₹1,40,038 crore between 2016 and 2023, and the settlement discussion around enrolled farmers and claim recipients.

- Ministry of Agriculture and Farmers Welfare / Press Information Bureau. PMFBY claim-processing reforms, including Digiclaim, crop-cutting experiment data through the CCE-Agri App, integration with the National Crop Insurance Portal, land-record integration, and measures aimed at timely and transparent claim settlement.

- PICC Property and Casualty Company Limited. 2024 Annual Results / Annual Report, used for the updated China section’s agriculture-insurance figures, including agriculture-insurance revenue, agriculture loss ratio, combined ratio, and agriculture-related claims volume.

Forecast probabilities are not certainties. Seasonal outcomes still depend on local factors such as irrigation, drainage, river systems, storage levels, land use, and preparedness.