Most UAE group placements carry a familiar line in the schedule:

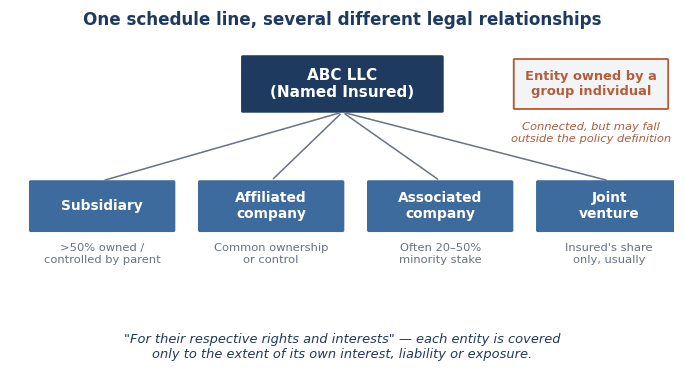

“[ABC LLC] and/or its subsidiary companies and/or associated companies and/or affiliated companies and/or joint ventures, as now existing or hereafter constituted, for their respective rights and interests.”

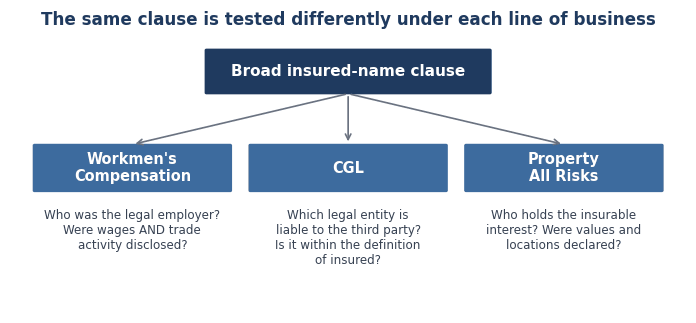

It reads like boilerplate. It is inserted to avoid missing group entities, accepted at placement, and rarely looked at again until a claim arrives. Then it can become the most contested line in the policy. It may decide whose employees are covered under a Workmen’s Compensation policy, which legal entity receives defence and indemnity under a CGL policy, and which group company can claim for damaged property or business interruption under a Property All Risks policy.

The wording is useful, and in group programmes it is often commercially necessary. But it is not a substitute for proper disclosure of entities, activities, payroll, turnover, locations, property values and joint venture interests.

Being in the same group is not enough

An American case illustrates the point well. In C.S. McCrossan Inc. v. Federal Insurance Co. (8th Cir. 2019), an insurer issued a crime policy to C.S. McCrossan Inc. covering McCrossan and any “Subsidiary,” defined by ownership or control of more than 50% of voting interests by the parent, directly or through subsidiaries. Part of the claimed loss was suffered by a property company that was wholly owned by a McCrossan individual, not by C.S. McCrossan Inc. or its subsidiaries. The court held that common ownership and management by McCrossan people, including board members, did not satisfy the policy’s test. The entity was not a defined subsidiary, so it was not insured, and its loss was not covered.

This was a US decision under a crime policy. This is not UAE precedent and should be treated as such. But the principle it illustrates travels well: a company does not become an insured merely because it is commercially connected to the group, managed by group people, or owned by individuals associated with the group. It must fall within the policy wording. When a UAE policy refers to subsidiaries, associated companies, affiliates and joint ventures, the claim question is often the same one that court asked: does this entity actually satisfy the words used in the policy?

Four terms that are not interchangeable

Because these words appear side by side in schedules, they look like standard market fillers. They are not. If the policy defines them, the definitions govern. If it does not, their meaning may have to be worked out from ordinary usage, statutory context, corporate records, and the commercial purpose of the placement.

A subsidiary usually means a company controlled by another company, typically through majority ownership. UAE Commercial Companies Law recognizes the holding company relationship in similar terms: control through shares or membership interests sufficient to control management and decisions.

An affiliated company is usually broader: a company that controls, is controlled by, or is under common ownership or control with another. A subsidiary is always an affiliate. An affiliate is not always a subsidiary.

An associated company is less precise. In business and accounting usage, it commonly means a significant minority stake, often in the 20% to 50% range. In an insurance schedule, the phrase may be argued more broadly or more narrowly depending on the policy context and the purpose of the placement.

A joint venture is different again. It is usually a cooperative arrangement between two or more parties for a defined enterprise, sharing resources, control, profits, and losses. It may be incorporated as a separate legal entity or exist only as a contract. Covering an insured’s interest in a joint venture is not always the same as covering the whole joint venture.

That last distinction is why the closing words of the clause, “for their respective rights and interests,” matter so much. They stop the wording from being read as unlimited group-wide cover. Each entity is protected only to the extent of its own legal or financial interest, liability, payroll, property or contractual exposure. The clause does not convert one group company’s asset, or liability, into another’s.

Workmen’s Compensation: wages are not the whole disclosure

The insurer at the time of claim would check for the name of legal employer of the injured worker, was that employer within the insured-name wording, were the wages and employee categories declared, and, most importantly, was the trade activity disclosed and accepted?

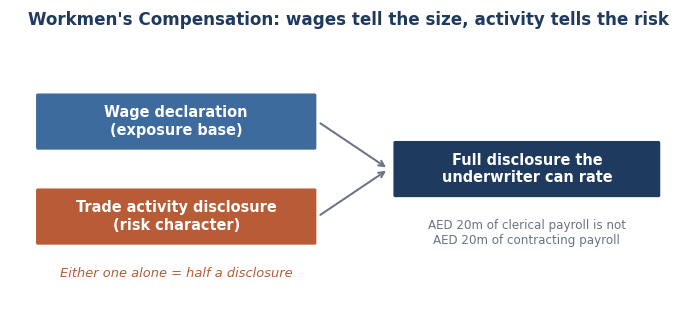

That last point about the trade activity is regularly underestimated. A client may say at claim stage: “We declared the full estimated annual wages for the group. The missed company’s payroll was included. So, the claim should be covered.” That may be partly true, but it does not answer the full underwriting question.

Wages are the exposure base. Trade activity is the risk character.

A wage roll tells the underwriter the size of the payroll. It does not tell the underwriter what the employees actually do. A clerical, trading or warehousing risk is not the same as MEP contracting, scaffolding, fabrication, marine repair, industrial maintenance, high-level cleaning or manpower supply.

Take a UAE group that buys a WC policy under the broad insured-name wording. At inception, the proposal describes the business as general trading and warehousing, with declared annual wages of AED 20 million. Mid-term, an employee of ABC Technical Contracting LLC, an omitted subsidiary, falls from height at a construction site. The insured points out that the wages were included in the overall estimate and the entity is part of the group. The insurer may ask a different question: was that entity’s contracting activity disclosed, rated, and accepted?

This is where the claim can become complicated. The issue is not merely the missing name. It is the missing risk profile behind the name. A broad insured-name clause may help where an entity was accidentally omitted from the schedule. It should not be treated as a cure for a materially different and undisclosed activity. How that plays out in each case will depend on the policy conditions, the materiality of the omission, and how the dispute is resolved under UAE law. But in WC insurance, a wage declaration without activity disclosure is only half a disclosure.

CGL: liability follows the legal entity

Under a Commercial General Liability policy, the question is different. It is not who employed the worker or who owned the asset. It is: Which legal entity is liable to the third party?

A group may operate under one commercial identity, but the law usually treats each company as a separate legal person. The company that owns the premises, signs the contract, supplies the product, performs the work or is named in the lawsuit may not be the entity that appears first in the schedule.

Suppose ABC LLC arranges a UAE CGL policy under broad insured name wording. A customer is injured at premises operated by ABC Leisure LLC. The lease, trade license, staff and operational control all sit with ABC Leisure LLC, but the schedule specifically names only ABC LLC. At claim stage, someone has to determine whether ABC Leisure LLC is a subsidiary, an affiliate, an associated company, or merely a company with common shareholders. Those are not the same thing, and the McCrossan principle shows why the difference can be decisive. If the entity that caused the injury or damage does not clearly fall within the definition of insured, the claim shifts from liability adjustment to coverage analysis.

The most uncertain area is joint ventures. A policy that simply says “and joint ventures” leaves open whether it covers the whole JV, only the named insured’s share, only declared JV activities, or only liabilities arising from the insured’s participation. These questions should be settled at placement, not after a serious third-party claim. A well-built CGL placement identifies the named insured, covered subsidiaries, additional insureds, joint ventures, contractual principals, cross-liability and severability provisions, and any exclusions affecting inter-company claims, supported by clear disclosure of turnover, activities, premises, products, contracts and territories.

Property All Risks: insurable interest and declared values

In a Property All Risks policy, the insured name performs yet another function. The question is not only who is named. It is: who has an insurable interest in the damaged property or financial loss?

A UAE group may hold assets across multiple entities. One company owns the building, another the stock, a third the machinery, and a fourth suffers the business interruption. A real estate SPV may own the premises while the trading company operates from them. If the policy is issued only in the parent’s name, the broad wording may become essential; without it, the SPV that actually owns the damaged property may struggle to prove it is an insured at all.

But even where an entity falls within the wording, the analysis does not end there. Was the location declared? Were the values included in the sum insured? Was the occupancy correctly disclosed? Was the BI value declared for the correct entity? Were mortgagee, loss payee or landlord interests noted? “For their respective rights and interests” does its quiet work here too: each insured recovers only to the extent of its own interest, subject to the declared values, limits, warranties and exclusions.

The gap between commercial and technical disclosure

Many coverage problems arise because the insured thinks in commercial terms while the policy responds in legal and technical terms. The client says, “It is all our group.” The insurer asks: which legal entity, which trade license, which activity, which payroll, which location, which JV interest? Both perspectives are understandable. The client sees one business. The insurer sees separate legal persons and separately rated exposures. That gap is where disputes live.

It is worth saying that the gap cuts both ways. An insurer that accepts a broad group wording, rates the risk on group-level wages or turnover, and asks no entity-level questions at placement may find it harder to challenge insured status later. Underwriters who want the protection of precise definitions should ask for entity schedules at quotation. Insurers should collect them. And claims teams should apply the wording as written, not treat every unnamed entity as a default declinature, I have personally experienced this question from the claims team asking the broker/client if the wages, turnover were considered for unnamed entities at the time of claim. The clause is a two-sided bargain, and it works best when both sides take it seriously before inception. There is challenge with online issued policies where there is less interaction between the insured/broker and the underwriter, the insured assumption will be that all their entities are covered under the broad insured name wordings and the claims team has no idea if the UW had actually considered for the wages and turnover for all the entities.

Tightening the wording

The standard clause can be supported with clarifying language. Note that “as now existing or hereafter constituted” may already sweep in future entities automatically, which is precisely why insurers often want a declaration condition attached. Illustrative approaches include:

For joint ventures:

“Joint ventures are covered only to the extent of the Insured’s legal or contractual interest therein and only in respect of activities declared to and accepted by Insurers, unless otherwise specifically agreed.”

For newly acquired or formed subsidiaries:

“Newly acquired or newly formed subsidiaries shall be automatically held covered for [30/60/90] days, subject to declaration to Insurers within such period and payment of any additional premium required.”

These are illustrative drafting concepts, not market-standard clauses. Each protects the insured from accidental gaps while preserving the insurer’s right to understand and rate the exposure.

Practical recommendations

For WC, do not collect only total annual wages. Collect entity-wise wages, employee categories, and trade activities. A missed subsidiary with clerical staff is not the same as a missed subsidiary doing contracting or high-risk manual work.

For CGL, identify which entity owns the premises, performs the operations, signs the contracts, supplies the products and may be sued. Liability follows legal responsibility, not internal group branding.

For Property All Risks, map property ownership and insurable interest. Buildings, stock, machinery, improvements, rent and BI exposure may sit in different entities.

For joint ventures, clarify at placement whether the policy covers the whole JV, only the insured’s share, or only liabilities arising from the insured’s participation.

For risk managers, maintain a simple group insurance schedule showing each entity, its ownership relationship, trade activity, payroll, turnover, property values, locations, and JV interests. It is the cheapest coverage-dispute prevention tool available.

Conclusion

The insured-name clause is not an administrative line. It is the bridge between the legal group structure and the insurance contract. Broad wording is valuable, but it is not a shortcut around proper disclosure. In WC, the missing issue may be the trade activity behind the payroll. In CGL, it may be the legal entity that is actually liable. In Property All Risks, it may be the entity that actually owns or bears the risk in the damaged property.

The lesson from McCrossan is simple: being connected to the insured is not the same as being insured. In group programmes, that question should be answered at placement, not asked for the first time after a claim.

Case reference: C.S. McCrossan Inc. v. Federal Insurance Co., 932 F.3d 1142 (8th Cir. 2019). Cited as an illustration of a general insurance principle, not as UAE precedent. This article discusses general market practice; coverage outcomes always depend on the actual policy wording, the claim facts and the applicable law.